Retirement Solutions

Defined Contribution Plans (DC Plans)

401(k)s and IRAs fall under the “defined contribution” umbrella. In these plans, the amount contributed is known or defined. Both employees and employers know the exact contributions made each year. However, the retirement benefit amount is uncertain because the employee chooses their investments, which can perform well or poorly.

Defined Benefit Plans (DB Plans)

DB Plans offer a specific or “defined” retirement benefit for each eligible employee. The focus is on the retirement benefit amount rather than the contributions. Pensions and cash balance plans are examples of DB Plans.

What is a cash balance plan?

Increasingly Used

The fastest-growing retirement plan in the country over the last 10 years.

“Hybrid Plan”

Commonly called a “hybrid plan” since it lives under the defined benefit umbrella but looks and feels like a 401(k). Often “bolted onto” a 401(k) to maximize tax deductions.

Contributions and Growth

Participants are provided with a set percentage of their yearly compensation (a “pay credit”) plus a guaranteed return on those funds (an “interest credit”).

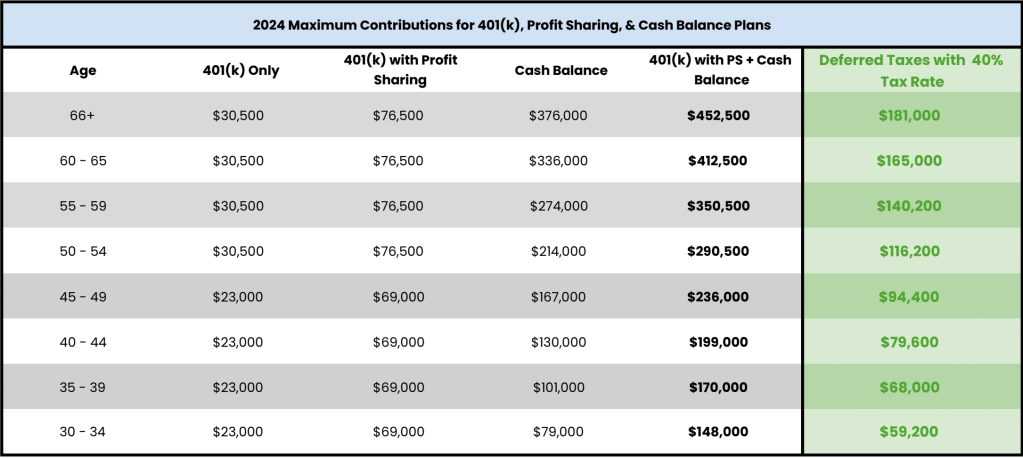

Combining a cash balance plan with a 401(k) profit sharing plan can produce the following tax deferrals:

Why Create a Cash Balance Plan?

Large Current and Future Tax Deductions

Cash balance plans offer substantial tax deductions. In some cases, tax deductions in a cash balance plan can be ten-times as large as those in a 401(k).

Tax-Free Investment Growth

The investments made with the CB contributions will grow tax-free until the participants sell those investments to fund their retirement.

Early Retirement Potential

Because a CB Plan allows you to, in some cases, contribute 10 times as much to your retirement accounts, aggressively contributing to your CB Plan super-charges your retirement saving which may make it possible for you to retire earlier and/or have a high standard of living in retirement.

Asset Protection

As an ERISA protected retirement plan, the entirety of the funds in your CB Plan are protected from creditors, litigation, and bankruptcy. This is a particularly important benefit for individuals in litigious industries such as healthcare and professional services.

Employee Retention

Plans can be designed to reward key employees with higher contributions. Also, the three-year vesting schedule means that an employee that leaves the company before their three-year anniversary would forfeit their CB contributions, and those contributions would stay in the CB Plan for the benefit of the business owners.

Easily Transferable

Once the owner closes the plan, or once an employee leaves the company, cash balance contributions can easily be rolled into an IRA and invested however the individual sees fit.